Short-Term Strength, Long-Term Pressure: What’s Driving the Grain Market

Mar 30, 2026

Zack Gardner

Grain Marketing & Origination Specialist

Short-Term Friendly, Long-Term Bearish

At the time of this writing, tomorrow is the March 31 Stocks and Prospective Plantings report. I think they should raise both corn and soybean acres, as the combination of corn and soybean acres from the USDA Ag Outlook Forum in February was one million acres less than last year’s corn/soybean acreage combo. The economics for cotton, rice, peanuts, and wheat are also worse than last year, which suggests we should be towards the higher end of corn and soybean acres as they look to plant commodities that lose less money. The second thing I will be looking at on the March 31st report will be the corn stocks and feed usage number. I think our feed usage number is overstated by 150 - 200 million bushels, which would also be bearish.

So Why Am I Short-Term Friendly?

The war in the Middle East is hugely inflationary. It’s mostly inflationary for crude oil and fertilizer, but inflationary stories cause the funds traders to buy all commodities as an inflation hedge. For example, despite hard red winter wheat having a 46 percent carryout (half of the wheat the U.S. produces this year, won’t get used this year) we are seeing an approximate $0.50 rally in wheat since the start of the war. Corn also has a 2.0+ billion-bushel carryout, and yet, corn is rallying as well. Also, I have to add the disclaimer that I am short-term friendly just as the market is trading the war headlines, and not actual grain fundamentals.

I Am Long-Term Bearish Though...

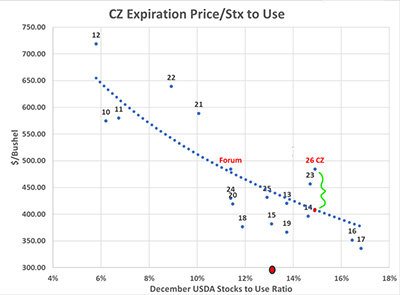

At some point, fundamentals will matter again. It might be this March 31st report, it might be a ceasefire agreement in the Middle East, or it could be a “normal” looking corn crop to show the funds that we can still produce corn despite the global fertilizer supply disruption. But at some point, the market should go back to trading fundamentals (our approximate two-billion-bushel corn carryout). Based off this chart, comparing our corn surplus to price, it shows December corn futures are about $0.70 overvalued.

Click to view graph.

As for soybeans, who knows! As it sits today, the U.S. has a 355-million-bushel carryout, or an 8.7 percent stocks-to-use ratio. Brazil is also wrapping-up harvest on another record soybean crop. Those are not exactly bullish, or even tight, fundamentals. The futures market is forward-thinking however and needs to price in the risk of a bullish biofuel policy or potentially more soybean sales to China that might wipe us out of old crop soybeans. I said the same thing a month ago about soybeans and I still think it reigns true today. I could make a case for soybeans being both $1.50 higher or $1.50 lower, depending on how some of these stories play out.

Grain Marketing & Origination Specialist

Short-Term Friendly, Long-Term Bearish

At the time of this writing, tomorrow is the March 31 Stocks and Prospective Plantings report. I think they should raise both corn and soybean acres, as the combination of corn and soybean acres from the USDA Ag Outlook Forum in February was one million acres less than last year’s corn/soybean acreage combo. The economics for cotton, rice, peanuts, and wheat are also worse than last year, which suggests we should be towards the higher end of corn and soybean acres as they look to plant commodities that lose less money. The second thing I will be looking at on the March 31st report will be the corn stocks and feed usage number. I think our feed usage number is overstated by 150 - 200 million bushels, which would also be bearish.

So Why Am I Short-Term Friendly?

The war in the Middle East is hugely inflationary. It’s mostly inflationary for crude oil and fertilizer, but inflationary stories cause the funds traders to buy all commodities as an inflation hedge. For example, despite hard red winter wheat having a 46 percent carryout (half of the wheat the U.S. produces this year, won’t get used this year) we are seeing an approximate $0.50 rally in wheat since the start of the war. Corn also has a 2.0+ billion-bushel carryout, and yet, corn is rallying as well. Also, I have to add the disclaimer that I am short-term friendly just as the market is trading the war headlines, and not actual grain fundamentals.

I Am Long-Term Bearish Though...

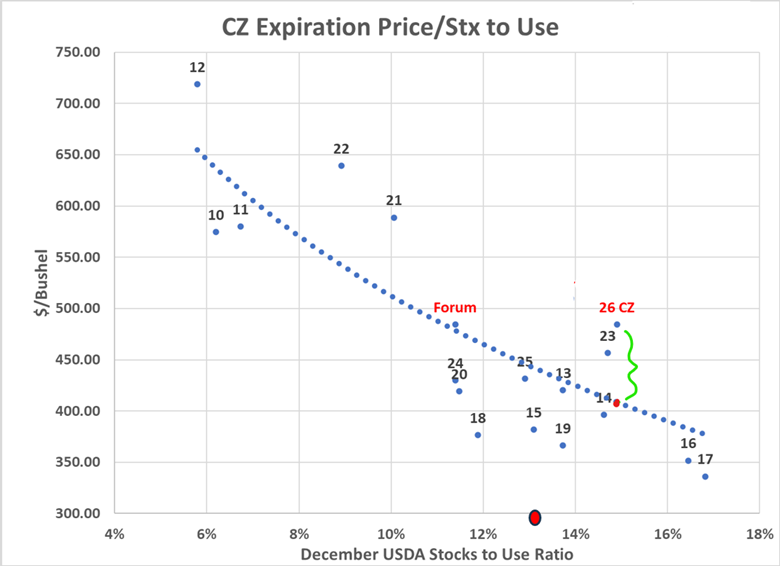

At some point, fundamentals will matter again. It might be this March 31st report, it might be a ceasefire agreement in the Middle East, or it could be a “normal” looking corn crop to show the funds that we can still produce corn despite the global fertilizer supply disruption. But at some point, the market should go back to trading fundamentals (our approximate two-billion-bushel corn carryout). Based off this chart, comparing our corn surplus to price, it shows December corn futures are about $0.70 overvalued.

Click to view graph.

As for soybeans, who knows! As it sits today, the U.S. has a 355-million-bushel carryout, or an 8.7 percent stocks-to-use ratio. Brazil is also wrapping-up harvest on another record soybean crop. Those are not exactly bullish, or even tight, fundamentals. The futures market is forward-thinking however and needs to price in the risk of a bullish biofuel policy or potentially more soybean sales to China that might wipe us out of old crop soybeans. I said the same thing a month ago about soybeans and I still think it reigns true today. I could make a case for soybeans being both $1.50 higher or $1.50 lower, depending on how some of these stories play out.